What do the assorted stakeholders in Indian banking – prospects, workers, shareholders, and the federal government – actually earn from the property of the monetary system? This deceptively easy query varieties the place to begin of our evaluation. By inspecting knowledge from the Reserve Financial institution of India (RBI) over the previous 25 years, we search to know how worth has been distributed throughout these teams and what it reveals in regards to the evolution of Indian banking.

Our findings, summarised within the accompanying charts, supply a revealing portrait of stability, inefficiency and asymmetry in worth creation. Regardless of large enlargement in scale and competitors, the distribution of returns throughout stakeholders has modified remarkably little. The banking system has grown over 25-fold in property; but the core economics – who positive factors, who bears danger, and who absorbs losses – stays largely the identical.

Mapping the stakeholders

The Indian banking system has 5 principal claimants on its worth creation:

Clients, comprising each debtors and depositors, who’re the first customers of the system’s monetary intermediation.

Staff and distributors, who extract returns by way of working bills – salaries, advantages, and funds for outsourced providers, expertise, and infrastructure.

Shareholders, who obtain residual earnings in spite of everything prices, taxes, and provisions.

The federal government, which earns taxes and dividends whereas additionally functioning as majority proprietor of public-sector banks (PSBs).

Defaulting debtors, a much less typical however very actual stakeholder class, who extract worth by way of credit score losses absorbed by banks.

Every stakeholder’s returns could be traced by way of particular monetary ratios that hyperlink the system’s steadiness sheet to its revenue distribution.

Measuring the claims

For workers and distributors, the related indicator is the working cost-to-average-assets ratio. Banks’ non-interest bills – largely employees and expertise prices – symbolize the combination compensation to these offering labour and operational help.

For the federal government, the tax-to-assets ratio captures its direct fiscal declare on banking earnings. This excludes the implicit return it earns through the statutory liquidity ratio (SLR) mechanism, which compels banks to carry a minimal share of deposits in authorities securities, thereby offering a steady supply of public financing.

Shareholders’ returns are greatest represented by the post-tax return on property (RoA) – the residual revenue in spite of everything different stakeholders have been paid.

Clients’ positive factors, nonetheless, are extra advanced to measure. The online curiosity margin (NIM) – the unfold between banks’ yield on property and their price of funds – serves as a proxy for the effectivity and competitiveness of the system. Over time, a extra environment friendly banking system ought to translate into narrower NIMs: debtors paying much less for credit score and depositors incomes extra on financial savings.

Lastly, credit score price provisioning displays the worth extracted by defaulting debtors. When banks put aside provisions for non-performing property, they successfully switch worth from shareholders (and, not directly, taxpayers in State-owned banks) to delinquent debtors.

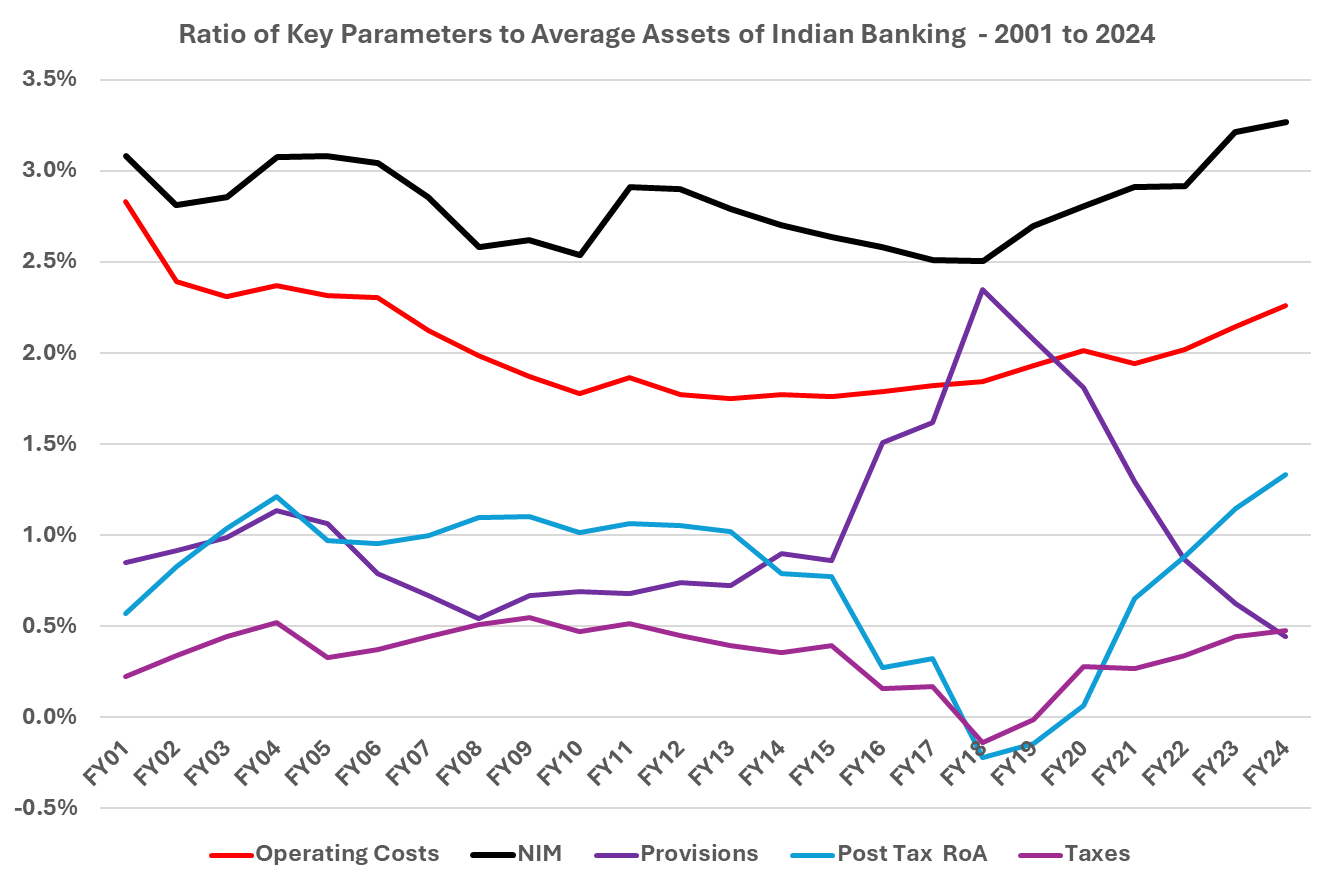

Determine 1 presents these 5 metrics for the Indian banking system between 2001 and 2024.

Determine 1. Ratio of key parameters to common property of Indian banking, 2001-2024

Supply: RBI, Authors computations.

Stability amid transformation

At first look, two options stand out: the extraordinary stability of NIMs and working prices.

The NIM for the Indian banking system has hovered between 2.5% and three% for practically 1 / 4 of a century, exceeding this vary solely briefly within the post-pandemic years. After reaching its decrease sure in 2018, margins have edged upwards once more – a mirrored image of the system’s shift in the direction of higher-yielding retail credit score, significantly unsecured client loans and bank cards, within the wake of the mid-2010s company bad-loan disaster.

This stability is placing when set in opposition to the size of change. Complete banking property in nominal phrases have surged from Rs. 11 trillion in 2000 to Rs. 281 trillion in 2024, a 25-fold improve. In the meantime, the construction of the business has been remodeled: private-sector banks, which accounted for roughly 10% of property in 2000, now maintain about 45%. But neither scale nor competitors seems to have compressed margins for purchasers.

The comparability with world friends is telling. Over 2020-24, US banks reported a median NIM of two.86%, whereas European and Chinese language banks operated at far thinner spreads of 1.45% and a pair of.18%, respectively. By this measure, Indian prospects – each debtors and depositors – proceed to pay much more for monetary intermediation.

Working prices present an identical sample of endurance. After productiveness positive factors within the early 2000s, when the cost-to-assets ratio fell from roughly 2.8% to 2%, the determine has barely budged. Since 2010, working prices have been anchored round 2%, rising barely to 2.2% after the pandemic.

Cross-country comparisons once more underline the puzzle. US banks function at roughly 2.5%, European friends at 1.4%, and Chinese language banks at simply 1%. The upper American ratio displays the inclusion of funding banks with cost-heavy buying and selling operations, however even adjusting for that, Indian banks seem inefficient given their a lot decrease issue prices – particularly labour and expertise.

Equally puzzling is the absence of economies of scale. Between 2010 and 2024, banking property expanded 6.5 instances in nominal phrases, but working prices didn’t decline. This implies that productiveness enhancements from digitisation and automation have been offset by rising bills, maybe in compliance, danger administration, or expertise upgradation.

The federal government’s regular take

The federal government’s specific fiscal return – taxes paid by banks – has remained remarkably steady at round 0.5% of property, besides throughout years of depressed earnings such because the late 2010s. However this measure understates the total extent of the State’s extraction from banking.

By the SLR regime, banks are presently required to carry no less than 18% of their deposits in authorities securities. In follow, holdings have persistently exceeded this ground, ranging between 22% and 25% in recent times. This ensures the federal government an assured and low-cost funding channel for its fiscal deficit.

The State’s twin function – as each regulator and majority proprietor of PSBs – compounds this. When credit score losses rise, the federal government’s tax revenues fall, and as a shareholder it suffers capital erosion, producing a double blow to public funds.

The risky two: Provisions and shareholder returns

Whereas NIMs, prices and taxes show spectacular fidelity, the credit score price and RoA metrics are much more risky – and intimately linked in a zero-sum style. Rising provisions sign deteriorating asset high quality, which immediately erodes shareholder returns.

In India’s case, the burden of credit score danger is borne primarily by shareholders, and to a lesser extent by the State by way of its possession of PSBs. In the course of the bad-loan cycle of the mid-2010s, provisioning spiked, earnings evaporated, and returns to fairness holders plunged. The information present how intervals of rising credit score prices coincide with sharp compressions in RoA and, by extension, in taxes paid.

This asymmetry – the place shareholders bear draw back danger whereas workers, distributors, and even prospects take pleasure in relative stability – underscores the peculiar danger distribution in Indian banking.

It may very well be argued that shareholders, together with the federal government, would tolerate the appreciable volatility stemming from credit score price provisioning, offered the inventory market delivered ample returns. For this assertion to carry, one would count on a constant upward development, or “score up,” in the important thing valuation metrics for the nation’s banking shares.

To check this speculation, we examined the 2 most typical metrics of fairness valuation – the Value-to-Earnings (P/E) ratio and the Value-to-Ebook Worth (P/BV) a number of – for the BankNifty index. Because the definitive value-weighted index for Indian financial institution equities, BankNifty affords probably the most dependable long-term knowledge for this sector. We analysed the annual averages of those two metrics from the index’s inception within the 2007 monetary yr by way of to 2025. The next evaluation of the trendlines reveals a placing consistency (Determine 2).

Determine 2:

Supply: AceEquity, Authors computations.

The charts illustrate that the P/E ratio for the interval remained largely range-bound, with a notable exception: a major spike between 2018 and 2020. This era coincided with the height of the Non-Performing Belongings (NPA) disaster, suggesting investor persistence throughout a systemic stress occasion. It’s pertinent to recall that this disaster was closely concentrated in PSBs, which necessitated an infusion of roughly Rs. 4 trillion in capital from the federal government.

The P/BV a number of demonstrates even higher stability, displaying no equal spike. Over your entire 18-year interval, the P/BV ratio averaged 2.21, with all annual figures remaining inside one normal deviation of this imply. The same image emerges for the P/E ratio; excluding the outlier years of the disaster, the common P/E sits at 16.5, with all different years falling inside one normal deviation.

In abstract, the established sample in these valuation metrics suggests a scarcity of re-rating for the banking sector’s equities. Banking inventory valuations are largely hovering across the identical degree noticed practically twenty years in the past. The evaluation concludes that the market has exhibited a outstanding neutrality: it has neither considerably rewarded nor materially penalised financial institution shareholders for the inherent earnings volatility they’ve borne.

Diverging paths: Public versus non-public

The system-wide averages masks profound structural variations between PSBs and private-sector banks. Over the previous quarter century, PSBs’ dominance has steadily waned: their share of whole banking property has declined from roughly 85% to about 55%. Personal banks have gained floor by way of superior expertise, buyer focus, and capital energy.

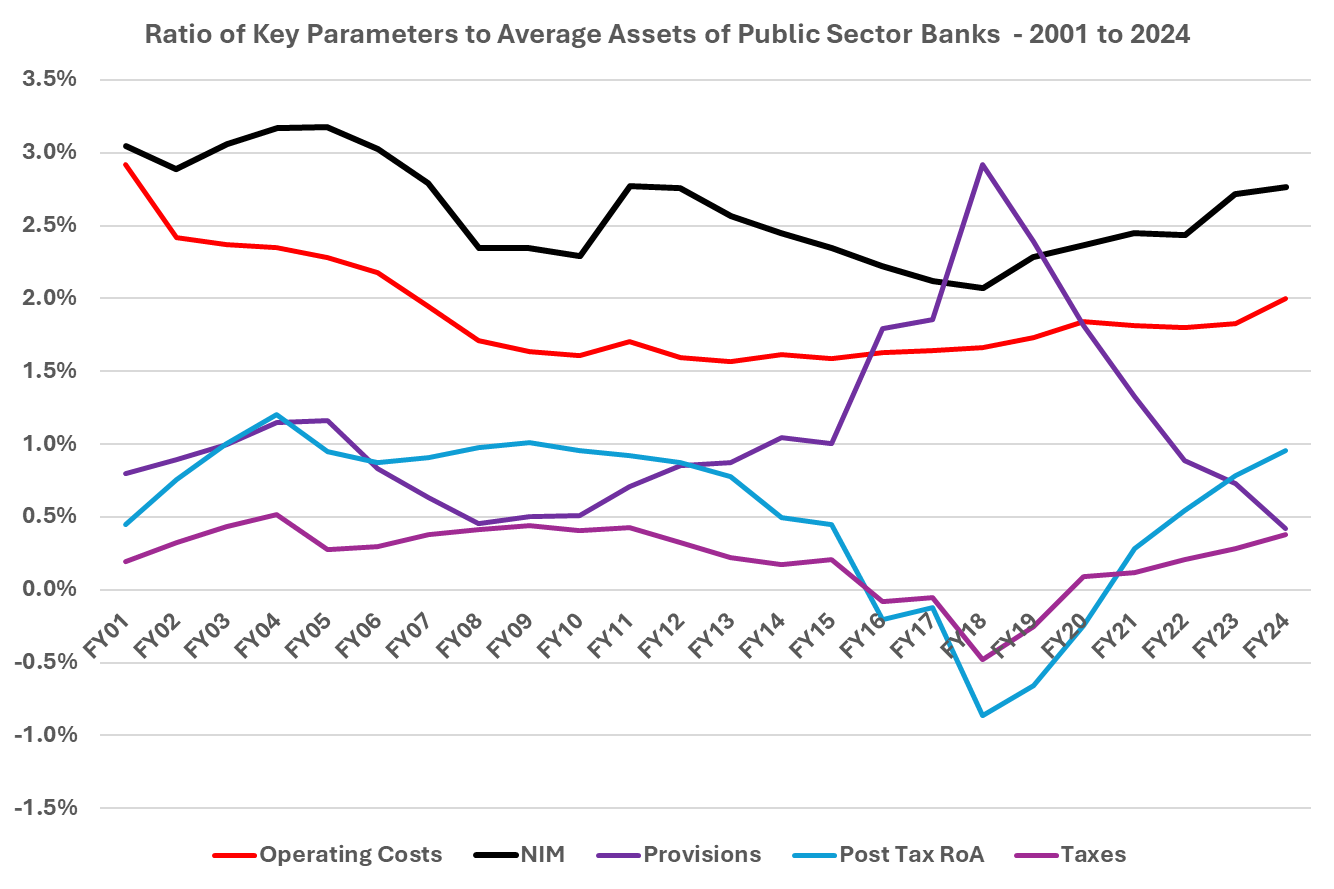

Determine 3 and Determine 4 under disaggregate the identical 5 metrics for PSBs and private-sector banks.

Determine 3. Ratio of key parameters to common property of PSBs, 2001-2024

Supply: RBI, Authors computations.

Public-sector banks

The parameters for PSBs broadly mirror the system-wide tendencies – unsurprising given their historic weight. Each NIMs and working prices stabilised after 2010, although at decrease ranges than the general system. NIMs fell from round 3% in 2001 to a band of two.1–2.7%, averaging roughly 2.5%. Since 2021, margins have edged up as PSBs adopted non-public friends into retail lending.

Working prices declined sharply within the early 2000s, from round 3% of property to 1.6% by 2010, largely attributable to IT adoption following a landmark settlement with worker unions within the late Nineteen Nineties. Thereafter, the ratio plateaued round 1.7%, rising barely after the pandemic.

The mid-2010s proved brutal for PSBs. The company bad-loan disaster triggered a wave of write-offs and provisioning, peaking at 3% of property in 2018. RoA, which had averaged 1% for years, turned detrimental in 2018 and 2019, recovering solely by 2024 to its historic norm.

The episode revealed each the fragility of PSB steadiness sheets and the fiscal implications of their possession. The federal government needed to inject substantial capital to revive solvency, absorbing a lot of the loss that may in any other case have fallen on non-public shareholders.

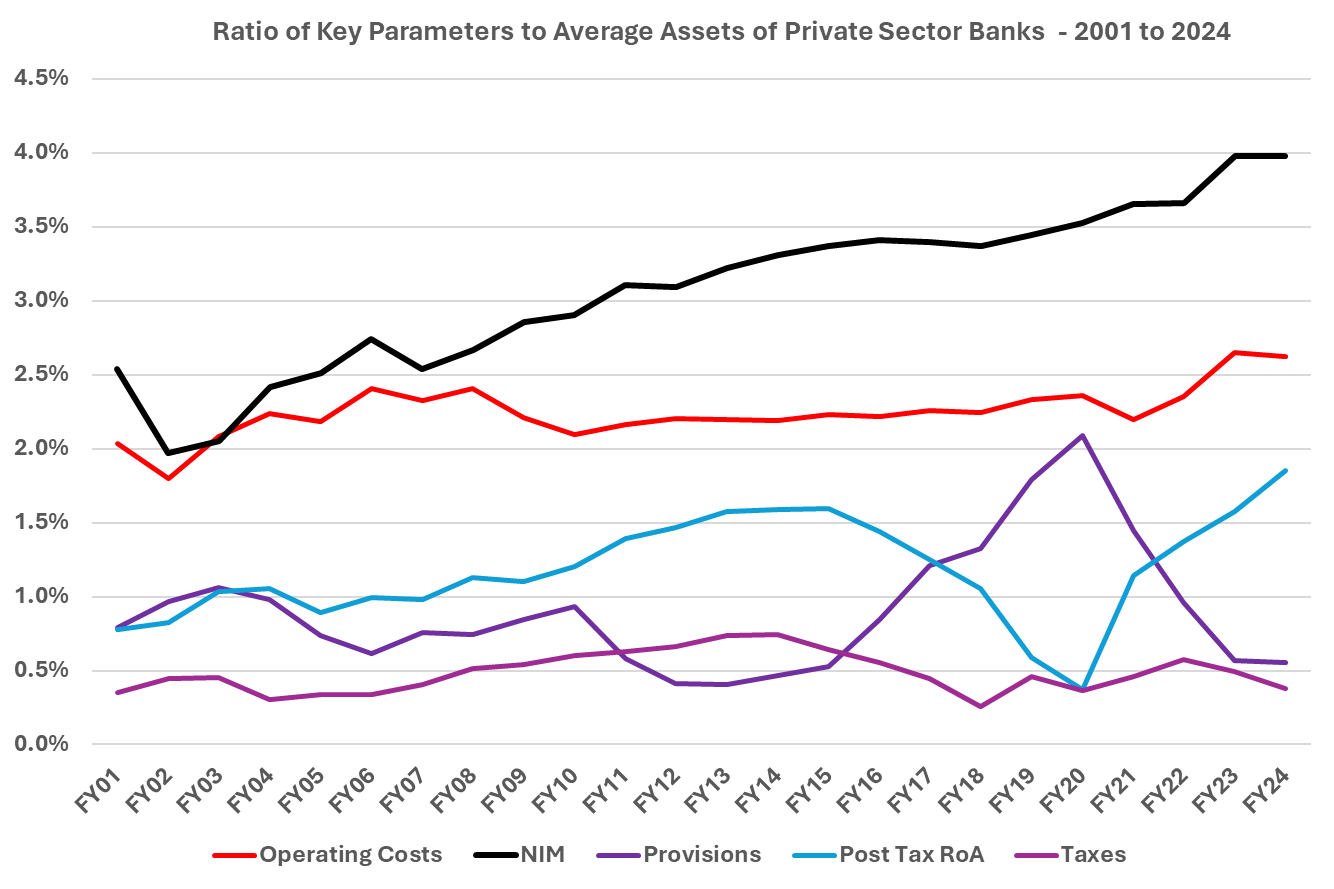

Determine 4. Ratio of key parameters to common property of private-sector banks, 2001-2024

Supply: RBI, Authors computations

Personal-sector banks

The trajectory of personal banks couldn’t be extra completely different. Within the early 2000s, their NIMs had been roughly at par with PSBs, round 2.5%. Thereafter, they rose steadily, reaching nearly 4% by 2024. The enlargement displays a strategic shift in the direction of high-yield retail lending, bank cards, and small-business financing – segments largely underserved by PSBs.

Working prices for personal banks have proven outstanding stability, averaging 2.2% of property throughout your entire interval. In contrast to PSBs, they didn’t expertise a dramatic early decline, having began from a extra environment friendly technological base. Nevertheless, regardless of quickly rising and a a lot larger share of client lending of their enterprise combine in comparison with their public sector friends, which has structurally larger working prices than business lending, these banks’ price ranges appear to be modestly larger. In recent times, nonetheless, their price ratios have inched up as they make investments closely in knowledge analytics, synthetic intelligence, and digital channels – expenditures which have but to translate into measurable productiveness positive factors.

Personal banks weathered the credit score cycle much better. Their peak provisioning degree, at 2% of property in 2019, was considerably decrease than that of PSBs. Consequently, their RoA dipped however by no means turned detrimental, indicating extra resilient profitability and superior danger administration.

1 / 4 century with out productiveness positive factors

Taken collectively, these metrics paint a sobering image. Over 25 years, Indian banking has expanded exponentially in measurement, adopted new applied sciences, and witnessed intense competitors – but its underlying effectivity and worth distribution have barely advanced.

The persistence of excessive NIMs and working prices means that productiveness positive factors haven’t been handed on to prospects within the type of decrease intermediation spreads. As a substitute, the advantages of progress have been absorbed by workers, distributors, and – in years of stability – by shareholders.

The credit score danger cycle stays the system’s Achilles’ heel. Each few years, poor underwriting, focus dangers, or financial downturns set off a surge in provisions that wipes out years of amassed earnings. In these episodes, the prices fall squarely on shareholders – and, within the case of PSBs, on taxpayers.

In the meantime, workers and distributors have loved probably the most constant extraction of worth. Their share of property, measured by working prices, has remained probably the most steady and among the many highest globally. In impact, the human and operational provide chain of Indian banking has been probably the most dependable beneficiary of its huge enlargement.

The broader implications

The evaluation raises a number of broader questions in regards to the construction and coverage design of Indian banking.

First, competitors has not delivered client profit. Regardless of new entrants, digitalisation, and coverage reforms, spreads have remained stubbornly excessive. This might replicate regulatory limitations, the dominance of huge incumbents, or the absence of price-based competitors in retail markets.

Second, scale has not yielded effectivity. The shortage of declining price ratios implies that organisational complexity, regulatory compliance, and expertise spending have offset any positive factors from measurement.

Third, danger stays asymmetrically distributed. The State, as each proprietor and regulator, shoulders disproportionate losses whereas non-public actors take pleasure in comparatively steady returns.

Lastly, the fiscal dimension – by way of SLR and recapitalisations – blurs the boundary between public finance and banking stability. The federal government successfully subsidises the system’s resilience whereas extracting regular tax and funding advantages.

Conclusion

In abstract, 1 / 4 century of information reveals a paradox. India’s banking system has grown, modernised, and diversified – but its basic economics stay frozen. Margins are sticky, prices are inflexible, and danger continues to be socialised. The system appears to be caught in a steady however low-quality equilibrium.

The true winners of this equilibrium look like workers and repair suppliers, whose claims on banking property have been probably the most dependable and least risky. The losers, recurrently, are the shareholders – and by extension, the Indian State.

For policymakers, regulators, and bankers alike, this could function a reminder: scale and expertise alone don’t assure effectivity. Except competitors interprets into decrease margins, and danger administration into steady profitability, the returns to stakeholders in Indian banking will stay as they’ve for the previous 25 years – erratically shared and structurally inert.

Leave a Reply