Abstract

- Overseas expertise corporations can’t be entrusted with assembly Europe’s rising digital wants. This contains American massive tech companies.

- Trump hardly ever hesitates to weaponise technological dependencies or assault the EU’s digital guidelines. A change of president sooner or later is unlikely to change these dynamics.

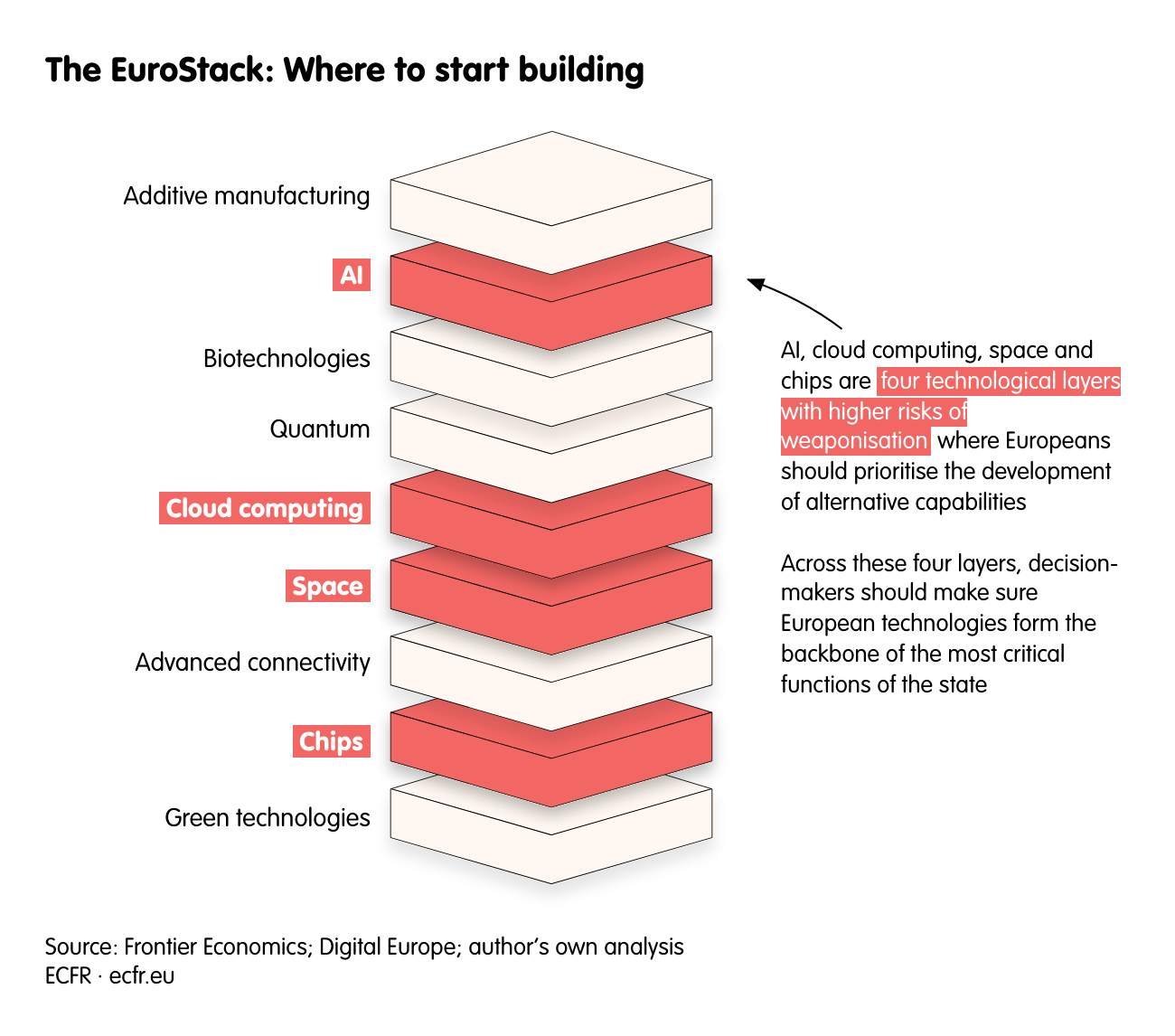

- The EU ought to construct an unbiased “stack” of applied sciences to defend itself from different powers weaponising tech towards it. Constructing this “EuroStack” should start the place such dangers are best, specifically within the domains of area, chips, cloud computing and AI.

- The EU doesn’t must assemble a wholly unbiased new tech ecosystem to strengthen its defences. As an alternative, it must construct “simply sufficient” capabilities in these key areas to extricate itself from its dependencies.

- American backlash towards this effort is probably going. However Europeans could make strategic concessions the place needed whereas retaining their eyes mounted on the sovereignty prize.

Liberation Day 2.0

It’s November 2026. President Donald Trump pronounces a brand new govt order on “Regulating Entry to American Expertise”. This resolution grants the president powers to declare a digital safety emergency and restrict or shut down US digital companies—like cloud companies, AI purposes and army software program—to international customers. The purported purpose is to safeguard nationwide safety and technological supremacy. The manager order cites European digital insurance policies and taxes as threats to American expertise safety. Requested how his transfer may have an effect on US allies, Trump remarks that “some nations is probably not our allies sooner or later”.

The reactions of US massive tech corporations are blended. Some reward the president for his “brave management”, whereas others vow to problem the manager order by way of all authorized avenues. The absence of readability within the legislation concerning govt powers over digital companies creates a fog of uncertainty.

In early 2027, the State Division pronounces sanctions towards “the suppression of free speech overseas”. Romanian prosecutors who charged former presidential candidate Calin Georgescu with plotting a coup are positioned on US sanctions lists. American digital corporations droop companies to those people, denying them entry to emails, social media accounts and cloud knowledge.

In the meantime, the Division of Commerce pronounces one other reform to its export management regime. The export of superior AI chips for knowledge centres now requires a person licensing settlement—from which different events can solely acquire an exemption in the event that they enter right into a expertise safety settlement with the US. Trump officers sign they’re eager to work out a such an settlement with the EU, however provided that the bloc drops its “unfair” regulatory obstacles towards US digital commerce. Semiconductor orders from EU gigafactories are placed on maintain.

After a tech dinner at Mar-a-Lago, the Trump administration declares that Meta and Apple is not going to be paying the fines totalling €700m lately levied on them by the European Fee. The White Home pronounces a legislation much like the European blocking statute that prohibits digital and tech corporations from complying with the EU’s digital laws and permits these corporations to get better damages.

Europe’s technological dependencies

Can we belief international expertise corporations to kind the spine of Europe’s digital transition? The digital realm’s unfold into just about all features of contemporary economies and societies means policymakers throughout the EU must be offering a solution. Worries about quite a few European dependencies on China are actually properly aired within the public debate. But, thus far, European decision-makers have solely simply began to grapple with what it means to be so deeply depending on American digital applied sciences.

Three US giants present 70% of Europe’s cloud computing infrastructure. American corporations dominate Europe’s cellphone working programs, and OpenAI’s ChatGPT has develop into synonymous with the idea of AI. Starlink represents a near-monopoly on Europe’s satellite tv for pc web companies, as does Nvidia in AI chips. The marketplace for social media—the digital squares of the European demos—are additionally dominated by US corporations Meta and X.

Till lately, Europe’s technological dependencies have been an issue confined to the world of antitrust and innovation coverage. However Trump’s second stint within the White Home has already remodeled Europe’s digital overreliance right into a geopolitical check. He has not hesitated to weaponise the financial and technological dependencies of others in pursuit of his personal aims.

In Ukraine, American officers threatened to close off Starlink satellite tv for pc companies except Kyiv agreed a minerals cope with Washington. The chief prosecutor of the Worldwide Prison Court docket misplaced entry to US digital companies after being focused by American sanctions. Towards Europe, Trump has weaponised each the risk of tariffs and the promise of tariff reduction in an try to drive the EU to water down its digital laws, which search to guard European residents from the unfair practices of expertise corporations.

This problem can be not restricted to Trump’s whims; a possible change in US management in 2028 is not going to essentially present reduction for Europe. In his final weeks in energy, President Joe Biden adopted the AI diffusion rule, which curtailed the variety of American AI chips that a lot of nations, together with EU member states, may import. There was no approach out of this for the 18 states affected: the administration was tired of hanging a cope with them nor did it want to punish them. Its purpose was to restrict leakage of chips to China, America’s major strategic competitor.

The US may additionally coerce Europe by imposing qualitative restrictions on exports to Europe. Within the realm of defence, for instance, Trump has introduced that any F-47 fighter jets bought to allied nations might be downgraded, citing potential future shifts in alliances. Trump has additionally mused that Nvidia Blackwell chips bought to China might be “enhanced in a adverse approach”. An analogous “qualitative restriction” strategy may embody promoting inferior expertise in satellite tv for pc networks, chips, digital companies or AI fashions.

The expertise below Biden ought to have been a pointy reminder that it isn’t simply Trump-style direct coercion that Europeans have to fret about. For any variety of causes, Europe would possibly discover itself confronted with service shutdowns, dealing with restrictions on absolutely the quantities of US digital applied sciences it could actually import, or denied parts important to creating digital applied sciences.

No trip to the rescue

The “Liberation Day 2.0” state of affairs additionally highlights the way in which wherein political weaponisation of expertise instantly impinges on the enterprise pursuits of the American giants. Conscious of those dangers, main expertise corporations have already made clear their intention to tackle the US administration the place its insurance policies threaten to intrude with their operations in Europe. As an illustration, Microsoft has dedicated to legally problem the US authorities if it mandates a shutdown of the corporate’s cloud companies in Europe. Amazon Net Providers unveiled a “European Sovereign Cloud” that might be “regionally managed within the EU, led by EU residents and topic to native legal guidelines”.

Nevertheless, Europeans can not depend on expertise corporations to face as much as this administration and its successors. Even when one assumes the very best of intentions, American corporations must abide by American laws and its extraterritorial results. Utilizing non-US subsidiaries or contractors overseas may additionally provide no answer: the federal government may lengthen restrictions to incorporate these and sue the father or mother firm at dwelling for potential breaches. For instance, US export management legal guidelines have a broad jurisdictional attain and may additionally apply to non-US corporations that manufacture items containing American expertise or parts. Equally, the 2018 CLOUD Act offers American authorities the facility to request cloud-stored knowledge even when these are situated overseas. Moreover, the Supreme Court docket lately restricted the flexibility of decrease courts to dam presidential orders, leading to fewer checks and balances on potential weaponisation. And that is earlier than expertise firm house owners contemplate the private threat of opposing presidential coverage: Elon Musk’s criticism of Trump’s finances invoice led to threats of subsidy cuts.

In practically any state of affairs, America’s expertise companies will at all times be within the weaker place within the face of a decided administration.

Might Europeans trip to their very own rescue and retaliate towards American weaponisation of expertise? Europe’s army dependency on the US makes this unbelievable, to place it calmly. This was one issue that mitigated towards retaliatory motion by the EU following Trump’s imposition of tariffs in early 2025—regardless of its personal potential energy as a global buying and selling bloc.

Constructing Europe’s expertise stack

Europeans can not depend on both the self-interest of American expertise corporations or (as issues at the moment stand) even themselves to maintain Europe’s computer systems on and its knowledge centres operating. They due to this fact must resolve learn how to de-risk from international digital applied sciences and construct different capacities of their very own.

The EuroStack

The “EuroStack” gives a prepared mannequin for European policymakers. This mannequin organises digital applied sciences right into a system of interconnected layers, displaying the relationships between several types of expertise. For instance, one can simply see how AI capabilities rely on cloud capabilities and, in flip, cloud capabilities rely on chips capabilities. The stack demystifies the digital transition, permitting policymakers (or certainly the lay individual) a clearer understanding of the place dependencies would possibly exist.

The thought of the EuroStack has been round for the final two years, largely confined to debates inside civil society and amongst antitrust specialists. However this 12 months political scientists Henry Farrell and Abraham Newman introduced it firmly into the realm of worldwide relations. They argued the EuroStack might be a part of the answer to withstanding geopolitical strain from each China and America.

Constructing a European digital stack is the logical political response for Europeans to the predicament they discover themselves in.

EuroStack for realists

Critics of the EuroStack level out that proudly owning each layer of the expertise stack can be counterproductive and prohibitively costly. That’s self-evident. However to de-risk from America’s digital applied sciences, the EU doesn’t must personal each layer throughout all sectors. To make the EuroStack a manageable and achievable endeavour, Europeans ought to observe three ideas.

First, it’s neither needed nor fascinating to interchange international oligopolies with European ones—this could solely generate its personal new set of financial and political issues. As an alternative, the target should be to construct viable European alternate options, which might compete available in the market alongside American suppliers.

Second, European applied sciences don’t should be adopted throughout all sectors directly. For instance, decision-makers ought to make sure that European applied sciences kind the spine of probably the most crucial capabilities of the state, like public administration and defence. However for sectors akin to agriculture, schooling and tourism, continued dependencies on American expertise would incur decrease threat. Even in these sectors, mitigation measures like selling the uptake of open-source options can additional cut back threat.

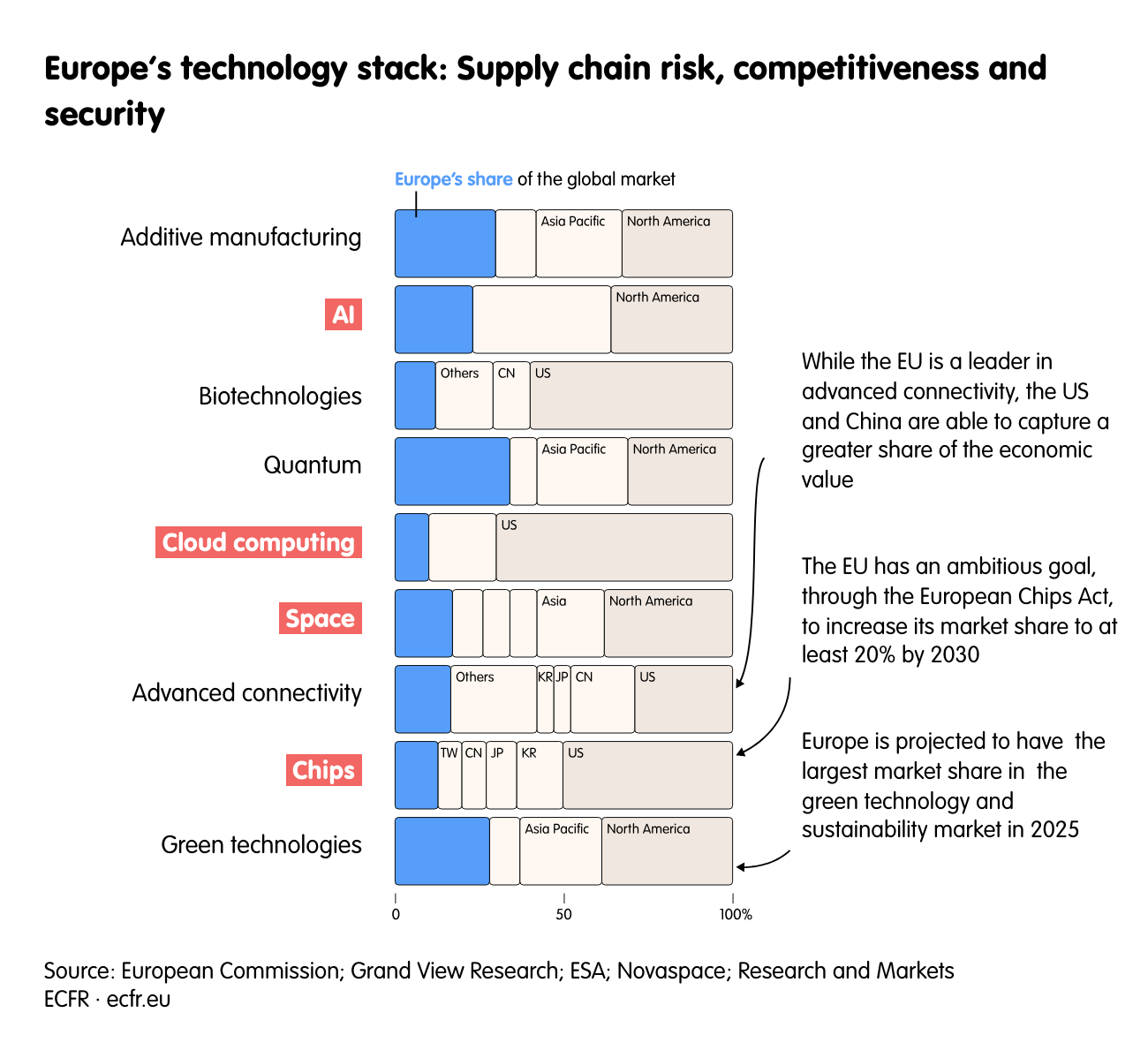

Third, the EU should focus efforts on the layers the place the weaponisation threat is best. For instance, with regards to superior connectivity (the networks and gadgets that allow quick and dependable communications), the EU’s publicity is low because of its substantial presence alongside the connectivity worth chain, excluding uncooked supplies and parts. The EU can be dwelling to Nokia and Ericsson, two world leaders in gear manufacturing. Consequently, constructing the EuroStack ought to begin with dedicating sources to different elements of the stack.

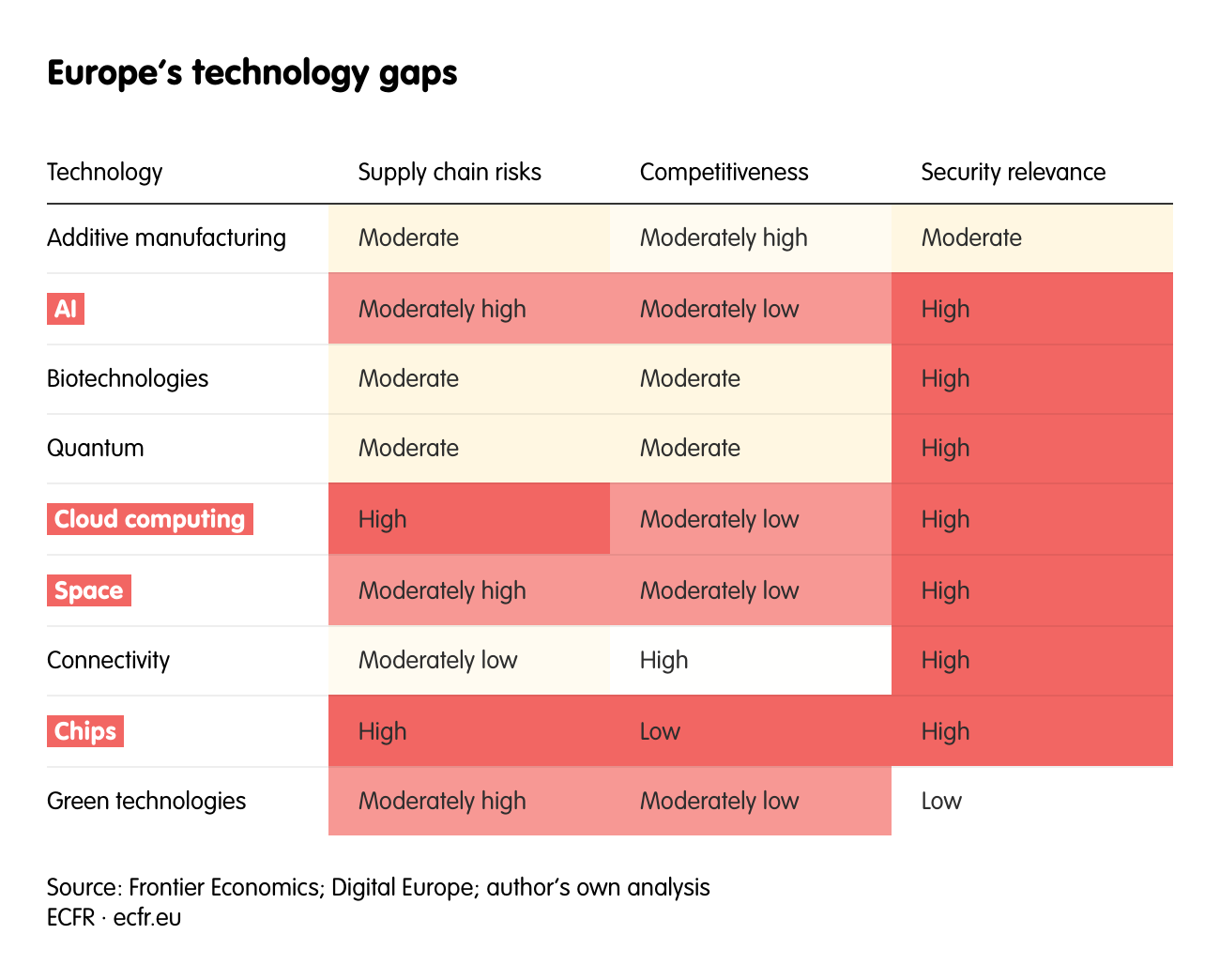

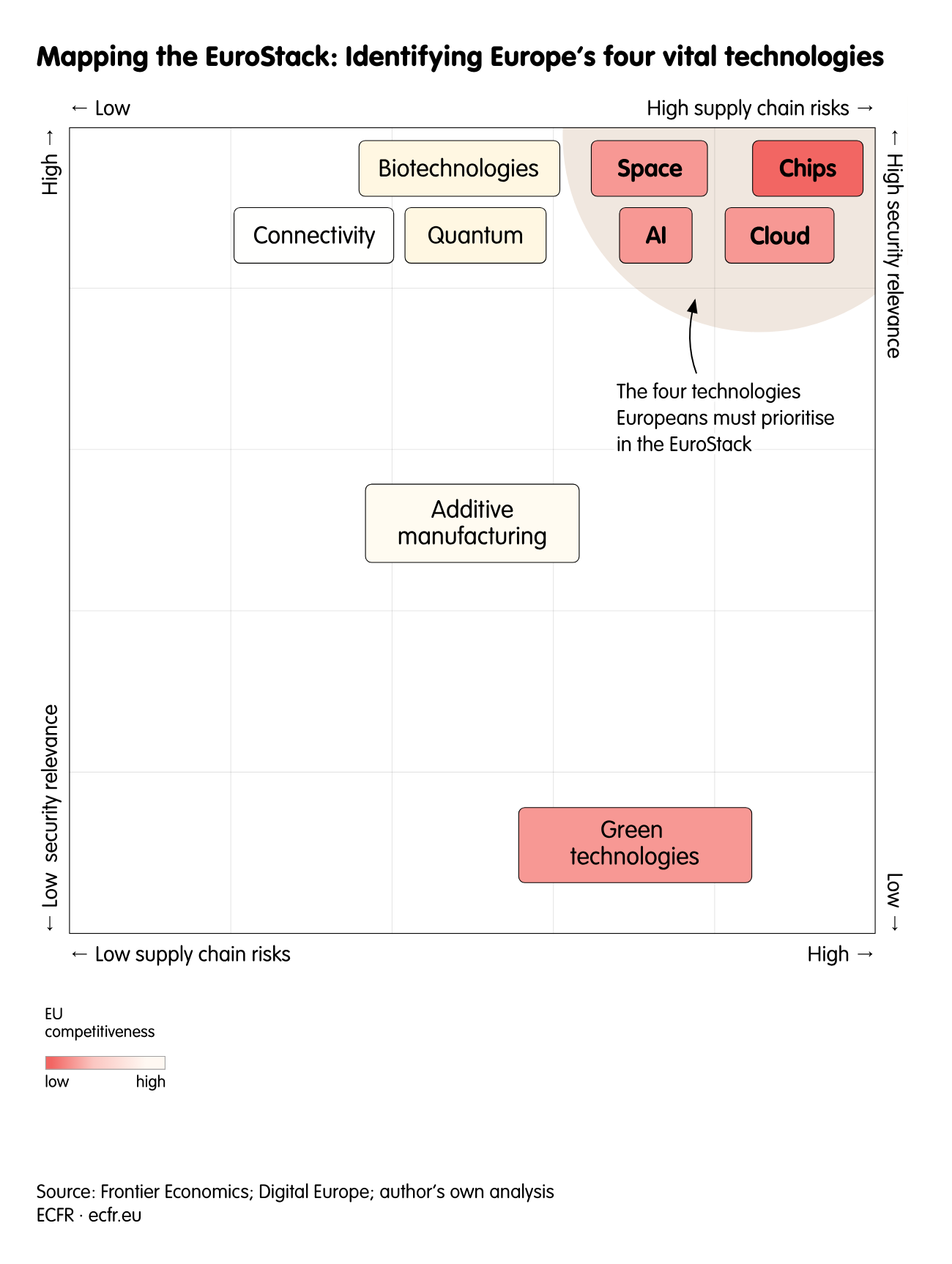

The 4 very important digital applied sciences for Europe

The EU and its member states ought to prioritise the event of, and entry to, different capabilities in 4 very important technological layers. These are: area, chips, cloud computing and AI. In these 4 applied sciences, the dangers are highest on account of their vulnerability to weaponisation, weak European competitiveness and significance in safety phrases due to the army capabilities they’ll present.

Various kinds of dependency exist inside every expertise. These are explored under, together with suggestions decision-makers ought to observe if they’re to reclaim sovereignty in digital applied sciences and avert weaponisation by the US and others.

House: The EuroStack’s lifeline

The chance

House is an important expertise for Europe’s competitiveness and safety: the Council of the EU this 12 months described area as “a constructing block for strategic autonomy”. It might probably present web entry in areas the place conventional infrastructure is missing and for locations experiencing emergencies. However the contribution of area applied sciences goes past connectivity and contains navigation administration (like GPS), environmental monitoring and scientific purposes. The worth of the area financial system is estimated to hit €1.6trn by 2033.

The EU is already dwelling to some distinguished area and satellite tv for pc producers, akin to Airbus and Thales. Nevertheless, it falls quick within the manufacturing of sure elements of the provision chain, akin to consumer terminals and navigation receivers, the place it’s depending on the US and Asia. The European House Coverage Institute has discovered that the EU is just not an area energy and lags behind the US, China and Russia as a result of it lacks autonomous capabilities.

The issue

One of the distinguished purposes of area applied sciences is within the space of defence and safety. In Ukraine, using area applied sciences to help army operations is unprecedented, primarily on account of Starlink satellites offered by Musk’s firm SpaceX. Ukraine’s deputy prime minister, Mykhailo Fedorov has mentioned: “Starlink is certainly the blood of our whole communication infrastructure”.

Nevertheless, Starlink is emblematic of the provision chain dangers inherent in area applied sciences and their potential weaponisation. When the US negotiated with Ukraine over entry to the nation’s crucial minerals, American officers threatened to chop the nation’s entry to Starlink. Musk himself mentioned this might trigger Ukraine’s “whole frontline [to] collapse”. When Polish international minister Radoslaw Sikorski shot again to say they may search for a brand new supplier, the American replied: “Be quiet, small man. [… T]right here is not any substitute for Starlink.”

The Starlink saga laid naked Europe’s dependencies within the realm of area expertise. With its 8,000 low cost satellites, SpaceX dominates the market. The EU’s response is the IRIS2 undertaking, which goals to place 290 satellites into service. Nevertheless, IRIS2 is not going to be operational earlier than 2031, whereas its scale and mission are a lot smaller. SpaceX can be seemingly indispensable for Europe’s launch wants. The European Ariane 6 rocket was handed over for the launch of a European climate satellite tv for pc, because the operator EUMETSAT most well-liked to utilize SpaceX’s launch companies and its reusable Falcon 9 rocket.

What to do about it

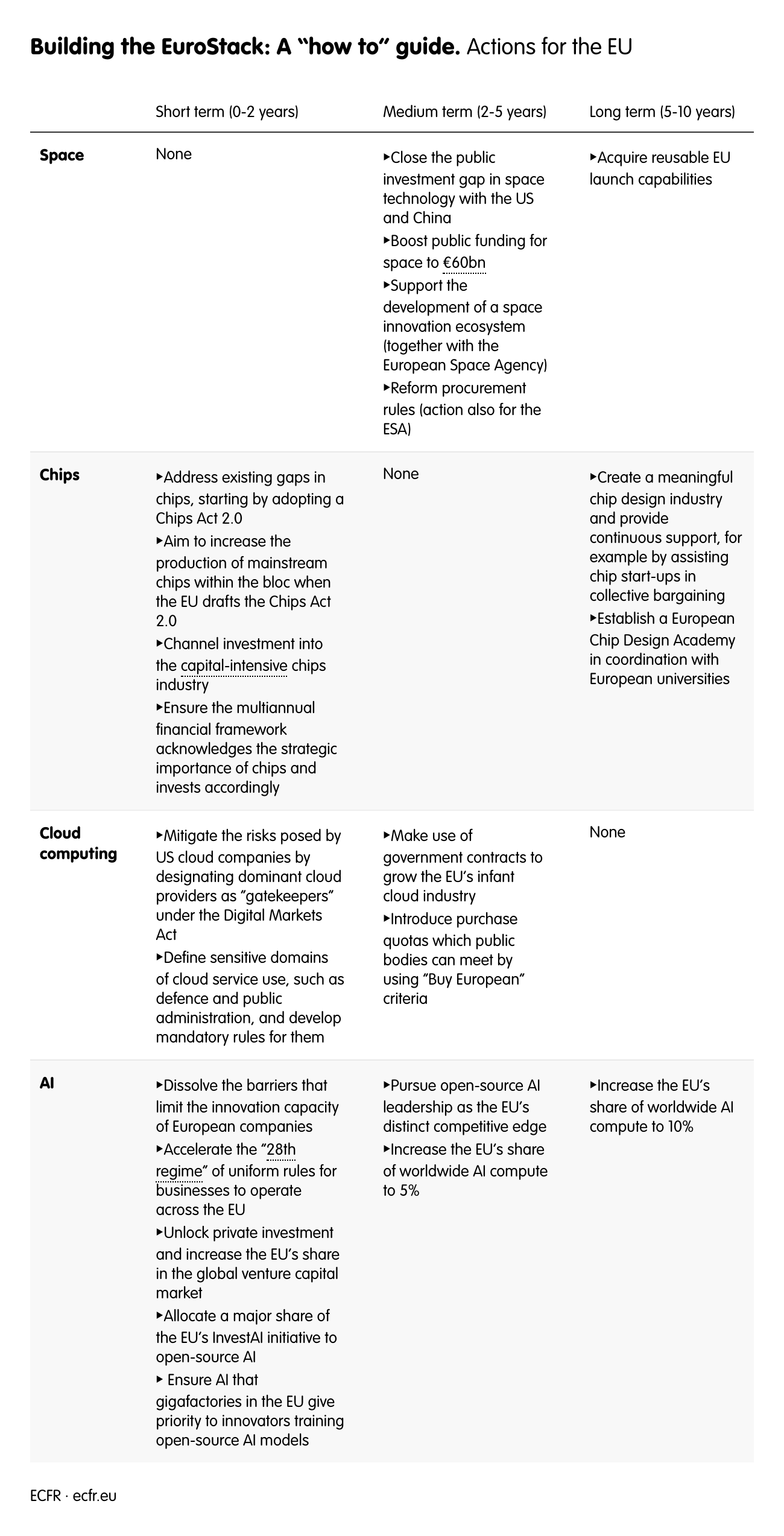

To develop into an area energy, the EU should shut the general public funding hole with the US and China.The EU and its member states invested lower than €12bn in area in 2023, whereas the US invested $66bn. Within the medium time period (2-5 years) the EU ought to goal to extend its public funding out there for area to €60bn.Such expenditure might be categorised below NATO’s dedication for allies to spend 5% of their GDP on core defence necessities and defence-related spending. Member states may additionally faucet into the ReArm Europe plan, which seeks to leverage €800bn by way of fiscal flexibility and the €150bn SAFE mortgage instrument.

In the identical time horizon (2-5 years), the EU and the European House Company (ESA) ought to help the event of an area innovation ecosystem. The emergence of personal area corporations providing cost-effective options represents a paradigm shift. Nevertheless, the Council of the EU famous in 2024 that personal sector engagement and funding within the European area financial system remains to be restricted. To reverse this pattern, Mario Draghi, creator of a significant report on European competitiveness, proposed an area fund that might allow the European Fee to behave as an “anchor buyer” and entice additional personal funding. Alongside this, each the EU and the ESA ought to reform their procurement guidelines. For the EU, quicker and extra versatile procurement guidelines are important to cater to the rhythm and wishes of start-up innovation. For the ESA, the rule of “geographical return”, which assures states that their nationwide contribution will correspond to contracts, needs to be abolished.

In the long run (5-10 years), the EU should purchase its personal reusable launch capabilities. Such a undertaking is already below approach: in November 2025, the ESA named a shortlist of potential corporations that might be contracted to construct the continent’s first reusable rocket launcher. That is a necessary step that can guarantee Europeans have entry to “simply sufficient” capabilities that can enable unconditional entry to area. Nevertheless, it is crucial that these capabilities are delivered on time and that delays are averted. (The IRIS2 satellite tv for pc undertaking famous earlier was initially deliberate to offer companies by 2027.) Taken collectively, these measures may assist construct the primary layer of the expertise stack and thus present safety for Europe towards weaponisation in area.

Chips: The EuroStack’s core

The chance

Chips are an indispensable aspect of Europe’s technological infrastructure. They’re important for a lot of different layers, akin to AI, and a number of different industries, together with defence, automotives and vitality. In distinction to a lot of the different layers of the expertise stack, the EU has acknowledged its chips dependencies and tried to alleviate them. In 2022, it adopted the European Chips Act, which goals for 20% of the world’s chip manufacturing to happen throughout the EU by 2030. Nevertheless, the act’s effectiveness is severely restricted. The European Court docket of Auditors reported the goal will virtually actually be missed. On present developments, the courtroom forecasts the EU is extra prone to obtain a worldwide market share of 11.3%. In response, the EU’s 27 member states printed a declaration because the Semicon Coalition in September 2025 calling for a extra bold and forward-looking chips act. This exhibits that Europe’s gradual progress has been recognised on the political stage, doubtlessly opening the way in which for decision-makers to agree efficient options to this downside.

The issue

Chips are additionally the stack expertise that has most frequently skilled disruption lately. In 2020, the covid-19 lockdowns led to shortages of Chinese language chips, which slowed down European automobile manufacturing. The US administration’s short-lived AI diffusion rule described earlier (and which was later dropped below the Trump administration) imposed strict quantitative limits on the variety of AI chips that some European nations may import. Most lately, China prolonged its restrictions on the export ofrare earth supplies used to create chips.

The strategic nature of chips and the frequent disruptions inside their provide chains make European chip capabilities important. Nevertheless, at the moment the EU possesses solely upstream capabilities, within the area of kit for chip fabrication because of the presence of the world-leading firm ASML. (No different such corporations are primarily based throughout the bloc.)

In the remainder of the chip provide chain, Europeans have just about no presence in any respect. EU states lack manufacturing capability (foundries) for probably the most superior chips and there aren’t any giant designers to compete with the likes of Nvidia or Qualcomm. Consequently, solely 1% of worldwide chip design is completed by European corporations, whereas the EU additionally accounts for lower than 10% of worldwide chip manufacturing.

What to do about it

Within the quick time period (0-2 years) the EU ought to tackle its current gaps, beginning by adopting a Chips Act 2.0.The European Court docket of Auditors notes that the unique Chips Act centered on cutting-edge chips, and thus missed trade demand for mainstream chips. However mainstream chips (within the vary of 65-90 nanometers) signify the majority of demand coming from European corporations, primarily within the automotive and industrial sectors. When it drafts the Chips Act 2.0, the EU ought to focus on rising the manufacturing of mainstream chips throughout the bloc. This may minimise additional dependencies on China and construct “simply sufficient” capabilities to assist it keep away from the weaponisation of different dependencies.

In the identical time horizon (0-2 years), the EU ought to channel funding into the capital-intensive chip trade. Funding for the European Chips Act got here primarily from member states’ state support. The EU should reinforce these efforts and be sure that its forthcoming multiannual monetary framework acknowledges the strategic significance of chips and invests accordingly. That being mentioned, within the present fiscal local weather public funding by itself is unlikely to strengthen the EU’s capabilities on this a part of the EuroStack. In AI, the personal sector pledged €150bn in funding till 2030, to high up the EU’s €50bn InvestAI initiative. Related pledges in chips will thus be required to ship the proper alerts to the remainder of the market.

Within the medium time period (5-10 years), the EU ought to goal to create a significant chip design trade. To realize this, it might want to guarantee an elevated variety of chip designers are skilled up throughout the European workforce. Presently, solely 6% of European STEM graduates are anticipated to enter the chip trade by 2030, and chip designers signify a fraction of this quantity. The EU ought to due to this fact set up a European Chip Design Academy in coordination with European universities. The academy would provide funding for related tutorial programmes and meet demand on this space.

Apart from nurturing expertise to develop the nascent chip design trade, the EU should present steady help, for instance by aiding start-ups, which can want collective bargaining energy to entry design parts which are offered by TSMC (Taiwan), Samsung (South Korea) and Intel (America). The EU ought to take these wants into consideration inside its Digital Partnership Agreements and act as a collective voice.

Cloud computing: The EuroStack’s bedrock

The chance

Europe’s computations and knowledge storage more and more happen “within the cloud”, making cloud computing the bedrock of the long run European expertise stack. In 2024, 52% of European companies made use of cloud companies; the European Fee goals to extend that determine to 75% by 2030. Cloud infrastructure is important for the event of different applied sciences, such because the “web of issues” and AI. Cloud computing has additionally develop into a core element for important state capabilities, from e-government to the conduct of army operations.

The issue

Regardless of the central function of the cloud, the EU market is “largely misplaced to US-based gamers”, in accordance to Draghi. Amazon Net Providers, Microsoft Azure and Google Cloud—often called the “hyperscalers”—management 70% of the European cloud market. In stark distinction, the most important European cloud suppliers, SAP and Deutsche Telekom, every account for two% of the EU market. In whole, European corporations management 15% of EU market share in 2025, a considerable drop from 29% in 2017.

The dominance of US cloud suppliers stems from their capacity to function like IKEA, in keeping with skilled Bert Hubert. Like the shop, they supply a service that’s all-encompassing, the place clients can discover what they should fulfil any want, on this case to construct IT options. These complete companies vary from knowledge storage and electronic mail options to AI instruments and even satellite tv for pc floor stations. Conversely, European cloud suppliers are solely capable of provide a subset of cloud companies. As Hubert places it, “nobody is considering a much less full IKEA”. The mixing of companies inside hyperscalers’ cloud ecosystems generates community results that make switching suppliers extra unlikely—and thus pose even harder competitors for Europeans wishing to catch up.

What to do about it

Pressing motion is required to construct the EuroStack’s cloud layer. Within the quick time period (0-2 years), the EU ought to search to mitigate the dangers posed by US cloud corporations by levelling the enjoying area for different suppliers. To do that, the EU ought to designate dominant cloud suppliers as “gatekeepers” below the Digital Markets Act. This might forestall anti-competitive practices akin to tying entry to cloud companies with their different companies and giving extra beneficial remedy to their very own cloud companies. The EU also needs to make use of its personal upcoming Cloud and AI Improvement Act to ban different practices akin to egress charges, which clients pay when shifting knowledge out of a cloud supplier’s community, and dismantle different synthetic obstacles to switching companies.

In the identical time span (0-2 years), the EU ought to outline delicate domains of cloud service use, akin to defence and public administration, and develop necessary guidelines for them. So as to make sure the safety, privateness and encryption of delicate info, cloud companies in these domains needs to be operated by European cloud suppliers. Whereas European suppliers are unlikely to match the sources of the hyperscalers, this measure would be sure that the EU and its member states select sovereign options in domains that matter probably the most. Policymakers in some member states have raised considerations in regards to the potential breach of worldwide commerce guidelines that such provisions would entail.[1] Nevertheless, the EU can totally adjust to the World Commerce Group’s Settlement on Authorities Procurement by making use of the exceptions granted by the settlement to procurement that’s “indispensable for nationwide safety”.

Within the medium time period (2-5 years), the EU should make use of presidency contracts to develop its toddler cloud trade. Public procurement represents round 15% of the EU’s annual GDP, a determine approximating to €2.5 trn. A dedication by governments to “purchase European” would redirect vital sources to homegrown cloud suppliers, which in flip is prone to result in extra aggressive services and products. That is additionally in step with Draghi’s suggestion to introduce express minimal quotas for native manufacturing in public procurement. This might assist member states develop into “launch clients” in new applied sciences. The EU ought to due to this fact introduce buy quotas which public our bodies can meet by utilizing “Purchase European” standards. It might probably do that both by revising the Public Procurement Directive, modifications to that are already deliberate for late 2026, or by way of the Cloud and AI Improvement Act,

AI: The EuroStack’s frontier

The chance

AI is prone to be probably the most transformative layer of the EuroStack. Its general-purpose nature means AI may reshape at this time’s industries and ship vital financial advantages. In science, for instance, the achievements of the AlphaFold mannequin might allow the invention of new medicines. In whole, AI’s adoption throughout economies may drive a 7% improve in world GDP over the following 10 years. AI can be set to rework the army sphere and improve standard and cyber defence capabilities by matching or exceeding human efficiency throughout army operations.

The issue

Regardless of the transformative potential of AI, the EU is reliant on the US for the chips and compute that AI requires in addition to for the AI fashions themselves. Chips make up just one a part of the compute layer, which additionally requires a software program element and the information centres that allow the event of AI fashions. The EU’s dependency on American AI chips and cloud companies has been already documented within the sections above. However, even when dedicated to buy AI chips from the US, the EU has been unable to construct its personal AI compute energy. This 12 months, the European Fee introduced a flagship AI gigafactories initiative. However, taken along with France’s AI knowledge centre ambitions, it will make up solely 2% of the world’s compute by 2027. Such capabilities will fall far quick in supporting an ecosystem of European frontier AI builders that may present extremely succesful fashions. The EU will due to this fact be pressured to import compute. At greatest, this could imply renting computational energy on demand; at worst, it might imply dropping European champions to US giants by way of acquisitions.

It’s the identical image with regards to AI fashions. Mistral AI—Europe’s final hope within the sector—represents 2% of the world’s giant language fashions (LLMs) market. Mistral AI additionally ranks backside with regards to functionality benchmarks vis-à-vis its American counterparts, and its funding is dwarfed by corporations akin to OpenAI. It’s indicative of the dearth of European AI capabilities that many EU member state governments have chosen to signal strategic partnerships with American AI mannequin suppliers as a substitute of with European suppliers. As an illustration, Estonia and Greece commissioned OpenAI to combine LLMs of their schooling programs whereas the European Parliament makes use of Anthropic’s Claude mannequin for its archives.

What to do about it

To construct the AI layer of the EuroStack, European policymakers should sort out dependencies in each AI compute and AI fashions.

Compute is a necessary means to the EU’s AI ends. Whereas Europe is unlikely to match America’s or China’s sources on this area, constructing a inventory of European private and non-private AI compute is important for safety functions. Recalling the necessity to construct a “reasonable”, deliverable EuroStack, the EU’s whole AI compute infrastructure doesn’t should be owned by Europeans to guard the bloc from weaponisation.

Within the medium time period (2-5 years), the EU ought to search to extend its share of worldwide AI compute to five%, and thence to 10% in the long run (5-10 years). This might enable EU entities to run some AI fashions regionally and securely. It could additionally seemingly allow the event of specialized fashions that the EU would want to retain management over—akin to in public administration, defence and in crucial industries.

Relating to AI fashions, a top-down strategy is not going to work. (A top-down strategy might be more practical in different elements of the expertise stack, akin to for chips and cloud computing.) As an alternative, the EU ought to goal to dissolve the obstacles which have restricted the innovation capacityof European corporations in AI(in addition to in different sectors). Within the quick time period (0-2 years), EU decision-makers ought to speed up the adoption and implementation of the “28th regime” of uniform guidelines for companies to function throughout the EU.

In the identical timeframe, the EU should unlock personal investments and improve its share within the world enterprise capital marketin order to draw funding for the capabilities that can make up the EuroStack. This may require that institutional buyers, akin to pension and insurance coverage funds, are incentivised to redirect belongings in direction of riskier enterprise capital.

Lastly, the EU ought to pursue open-source AI management as its distinct edge within the medium time period (2-5 years). A research carried out by MIT and start-up Hugging Face confirmed that the full downloads of Chinese language open-source AI fashions have surpassed downloads from American corporations.

The EU ought to goal for European open-source AI fashions to develop into the fashions of selection on this essential market. Open-source AI would allow market entry for Europe’s low-resource actors and allow better AI adoption by way of customisation. To ship the proper alerts to the market, the EU ought to allocate a significant share of its InvestAI initiative to open-source AI within the quick time period(0-2 years).In the identical time interval, the EU’s AI gigafactories also needs to give precedence to innovators coaching open-source AI fashions.

The playing cards are stacked

Because the saying goes: if the playing cards are stacked towards you, reshuffle the deck. But when applied sciences are stacked towards you, it’s time to make a deck of your personal.

The EU has out of the blue discovered itself struggling to outlive in a worldwide order dominated by worldwide energy play. The foundations of the sport have modified, with direct implications for the EU’s dependencies in commerce and expertise. Since Trump’s return to energy, a lot of the world has been transfixed by his tariff exploits: the weaponisation of commerce dependencies has develop into ever-clearer to governments world wide. However expertise dependencies stay much less examined. The prospect of a “Liberation Day 2.0” exhibits how believable expertise weaponisation might be. The use and misuse of technological dependencies is already with us, from export controls on chips to Starlink’s function in Ukraine. The one approach for Europe to guard itself from these assaults is to construct its personal unbiased stack of applied sciences. Sovereignty, on this regard, is just not about limiting however about enabling. European alternate options can deliver selection for shoppers, residents and states; they’ll compete alongside American suppliers.

The event of a EuroStack is prone to provoke reactions from the opposite facet of the Atlantic. To minimise frictions, Europeans may undertake these measures with out making sturdy reference to US dependencies—and certainly with out even making reference to a EuroStack. Even so, measures akin to choice for European corporations in public procurement are unlikely to go unnoticed. In such instances, Europeans may get what they want with a little bit of give and take, akin to by offering strategic concessions the place needed. As an illustration, the EU may soothe Trumpian ire by serving to America hold its benefits particularly areas, akin to cutting-edge chips and AI compute infrastructure. Europeans have been right here earlier than: when the EU’s Galileo undertaking sought to develop different options to satellite tv for pc navigation, the bloc made strategic concessions to the US to alleviate tensions. However finally it was nonetheless capable of develop its personal different capabilities.

The high-level Summit on European Digital Sovereignty which occurred in November 2025 recognised the significance of discovering options to strengthen sovereignty on this space. However now Europeans should flip their political intentions into real-world capabilities. On this pursuit, they may should be selective, and above all reasonable. New and stronger capabilities can’t be constructed in a single day throughout all layers. Choice-makers should start the place the dangers of weaponisation are best, the EU’s competitiveness scores poorly, and defence safety issues are a priority. House, chips, cloud computing and AI are the locations to start out. Success requires the EU and its member states to view the event of different capacities in these applied sciences as important funding that can improve each their financial and army safety. In the end, the query is just not whether or not Europeans can afford to construct their very own expertise stack, however whether or not they can afford to not.

Concerning the creator

Giorgos Verdi is a coverage fellow with the European Energy programme on the European Council on Overseas Relations. His analysis focuses on the implications of crucial and rising applied sciences for the EU’s competitiveness, financial safety and international coverage.

Acknowledgments

This coverage transient was supported by funding from Luminate Initiatives Restricted. The creator want to thank Adam Harrison for his sharp suggestions and edits that helped to make this transient higher. The creator would additionally prefer to thank Chris Eichberger and Nastassia Zenovich for his or her invaluable help in shaping the visible identification of the transient in addition to Nele Anders and Mireia Faro Sarrats for his or her help on the advocacy entrance.

[1] Writer’s conversations with member state officers, July 2025.

The European Council on Overseas Relations doesn’t take collective positions. ECFR publications solely signify the views of their particular person authors.

Leave a Reply